Actuarial gains and losses on fund assets in 2022

Actuarial gains and losses on fund assets amount to €9,295 million for 2022. They mainly result from a €3,737 million change in France and a €5,505 million change in the United Kingdom, in an environment of falling bond and equity markets.

Net employee benefit liability at 31 December 2022

The net liability at 31 December 2022 amounted to €16,346 million, including:

- €16,656 million in France;

- €(638) million in the United Kingdom, reflecting recognition by EDF Energy of surplus funding on its EDFG pension scheme, totalling €658 million compared to €2,733 million at 31 December 2021. This surplus funding, which has decreased due to the negative performance by fund assets given substantial interest rate increases over the period, is recognised in balance sheet assets under “non-current financial assets”.

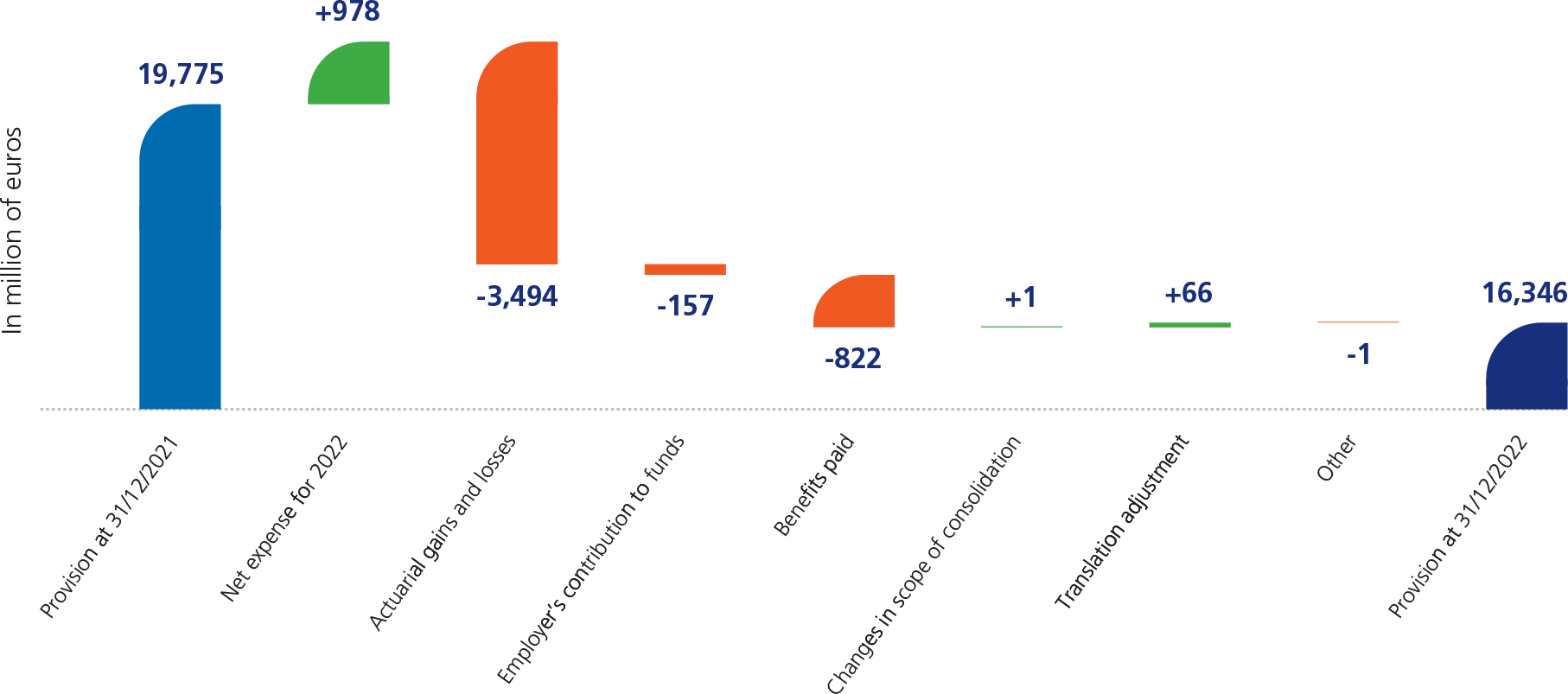

Changesin the net liability in 2022 were as follows:

This graph shows the changes in the net liability in 2022 were as follows:

Provision at 31/12/2021: 19,775 million of euros

Net expense for 2022: +978 million of euros

Actuarial gains and losses: - 3,494 million of euros

Employer’s contribution to fund: -157 million of euros

Benefits paid: -822 million of euros

Changes in scope of consolidation: +1 million of euros

Translation adjustment: +66 million of euros

Other: - 1 million of euros

Provisions at 31/12/2022: 16,346 million of euros

16.1.2 Actuarial assumptions and sensitivity analyses

The followingactuarial assumptionsareused:

|

|

|

|||

|---|---|---|---|---|

| (in %) | 31/12/2022 | 31/12/2021 | 31/12/2022 | 31/12/2021 |

| Discount rate/rate of return on assets(1) | 3.90% | 1.30% | 4.75% | 1.90% |

| Inflation rate | 2.30% | 1.70% | 2.90% | 2.95% |

| Wage increase rate(2) | 3.70% | 2.80% | 2.65% | 2.70% |

(1) The interest income generated by assets is calculated using the discount rate. The difference between this interest income and the real return on assets is recorded in actuarial gains and losses in equity.

(2) Average wage increase rate, includinginflation and projected overa full career.

The discount rate used for employee benefit obligations is determined by applying the yield rate on high-quality corporate bonds of appropriate duration to maturities corresponding to the future disbursements resulting from these obligations. For longer durations, the calculation also takes into consideration data from a wider selection of corporate bonds adjusted for comparability with the high-quality bonds, given the smaller panel of bonds with these durations since 2017.

Changes in the economic and market parameters used have led the Group to set the nominal discount rate in France at 3.90% at 31 December 2022 (1.30% at 31 December 2021). The increase in the discount rate essentially relates to the increase in risk-free rates observedin2022.

The inflation assumption is based on an inflation curve constructed from economic forecasts and inflation-indexed market products. As a result of changes in the

economic and market parameters, the assumed average inflation rate used as the Group’s benchmark for Euro zonecountriesis2.30% at 31 December 2022 (1.70% at 31 December 2021).

The pay rise agreements signed in 2022 have been taken into consideration in calculating the obligations. For 2024 and subsequent years, the wage laws referred to for these calculations are based on average wage increases observed in recent years (adjusted for non-recurring effects).

The mortality table used to calculate obligations is based on the INSEE 2013-2070 generation table (produced by the French statistics office), corrected for differences in mortality between the general French population and the population covered by the IEG regime.

Sensitivity analyses on the amount of the obligations are as follows:

| 31/12/2022 | ||

|---|---|---|

| (in millions of euros) | ||

| Impact of a 25bp increase or decrease in the discount rate | (1,066)/ 1,144 | (269)/ 256 |

| Impact of a 25bp increase or decrease in the inflation rate | 1,115/ (1,043) | 235/ (238) |

| Impact of a 25bp increase or decrease in the wage increase rate | 1,028/ (964) | n.a |

n.a:not applicable.